October 19, 2023

/

By Dominque Feloss, program associate

Postsecondary education- including certifications, 2-year degrees, 4-year degrees, and graduate degrees- are still impactful ways to achieve economic mobility. associate degree adds about $7,300 to a high school graduate’s annual income, while earning a bachelor’s degree adds $26,000 annually (Asset Funders). However, as the cost of education has risen and more people from low-wealth families have pursued postsecondary education, student loan debt has ballooned.

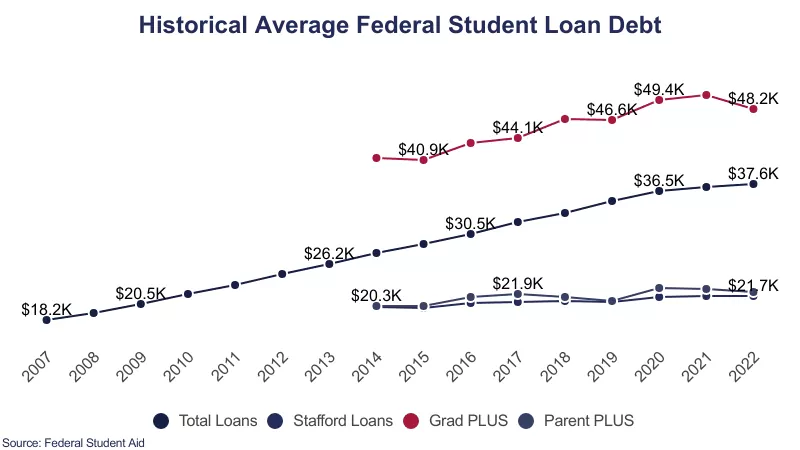

As of July 2023, the outstanding student loan debt in the United States has reached more than $1.77 trillion amongst the 43 million Americans who currently hold federal student loans.

In Georgia, the average student debt is $41,951-higher than the national average. Racial inequity also plays a significant role in the amount of debt that a student has accumulated. According to the National Center for Education Statistics, Black degree holders have an average of $52,000 in student loans, and 45% of this debt is from graduate school. The median value of unpaid student loans held by Black borrowers is $7,000 more than that of white borrowers (Asset Funders). In Atlanta, the median net worth of white households in Atlanta is 46 times the median net worth of Black households (Financial Health and Wealth Dashboard). The racial wealth gap both causes disparities in student debt and grows due to those disparities, creating a vicious cycle for people trying to get ahead.

As student loan borrowers prepare to resume paying their loans back this month, after a long pandemic pause, economists are unsure about the size of the impact on our economy but predict it will contribute to continued economic struggle and uncertainty. (CNBC)

The average borrower pays $200 and up a month on their student loans (Best Colleges). It’s fair to assume that the resumption of payments will hurt borrowers who are already struggling to pay their bills significantly. Many people have seen their rents, transportation, food, and other costs increase in relation to their wages since before the pandemic, and an additional $200 monthly expense will likely cause families to find ways to cut their budgets.

There are programs to help these families:

The Saving on a Valuable Education (SAVE) program is an income-driven repayment (IDR) plan that calculates monthly payments based on the amount of money that you make and the size of your family. An estimated 1 million low-income borrowers would quality for a zero monthly student loan payment through the SAVE program. Introduced by the Biden administration in August 2023, SAVE replaced the Revised Pay As You Earn (REPAYE) plan. Borrowers already enrolled in REPAYE are automatically enrolled in the SAVE plan (Investopedia); others should visit the Federal Student Aid website to learn more and apply.

Another option for nonprofit partners, in particular, may qualify for, is the Public Service Loan Forgiveness Program (PSLF). Borrowers must be employed by a government or not-for-profit organization to qualify for PSLF, which forgives student loans once qualifications, including making the equivalent of 120 qualifying monthly payments under an accepted repayment plan, are met. Borrowers can find more information on the Federal Student Aid website.

There are also many borrowers who are left out of these and other forgiveness and repayment plans. To address the gap in assistance, the Community Foundation has launched a Student Loan Debt Pilot Program. While the pilot program application has closed for 2023, the Foundation is raising money to continue this program in 2024 and beyond. Donors and community members interested in supporting this program can make a donation here or contact our philanthropic team.

Categories

- Arts, Culture and Creative Enterprises14

- Book Club26

- Community110

- COVID-1934

- Donor Stories57

- Events32

- Great Grant Stories65

- Higher Ground169

- Housing and Neighborhoods30

- Impact Investing38

- Income and Wealth20

- Media22

- News163

- Nonprofits39

- Philanthropic Resources184

- Place-focused8

- Power and Leadership9

- Press Releases100

- Publications87

- TogetherATL27

- Uncategorized426